Fulcrum's Diversified Absolute Return Fund added 2.04% in November. With this uptick, year-to-date performance rose to 12.80%.

The fund which was incorporated in July 2015 has $267 million in assets. The strategy includes investing in several asset categories, including bonds, equities, currencies, and commodities.

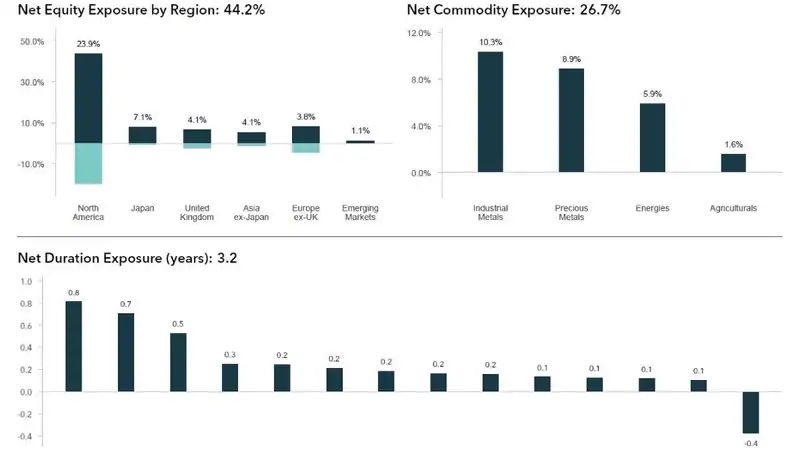

Performance Review

Managers analyze performance across three strategies: Discretionary Macro (DA), Diversifying Strategies (DS), and Dynamic Asset Allocation (DAA). During the month, DM and DS brought most of the performance contribution, while DAA was almost flat.

Also see: Fulcrum Income Fund Delivers Best Month Of 2025 With +3.2% Gain In September

The main issue with DAA input was concerns from AI sentiment, and talks about its overvaluation. The result was a reevaluation of long equity positions. However, by the end of the month, positive contributions from fixed income and commodities offset this decline.

Mid-November witnessed increased volatility, when active hedge trading proved beneficial. DA strategies finished the month on a positive note, aided by currency price trends.

The manager noted a strong month for DM strategies, with most of the strategy sub-categories being positive. The manager emphasized long positions in gold and silver as top contributors. Despite prices falling in the middle of the month, they recovered and pushed higher towards the end of November. Besides gold and silver, a long equity position from the UK element of the portfolio was a driver of positive performance. The position was also increased ahead of the new UK budget implementation. Another positive for the DM strategy was a new Japan equity long position based on the Nikkei 225 Stock Average Index. The fund's opinion was that the index had already net sold for too long, which proved correct. This was complemented by positives from a long position in Japanese yen.